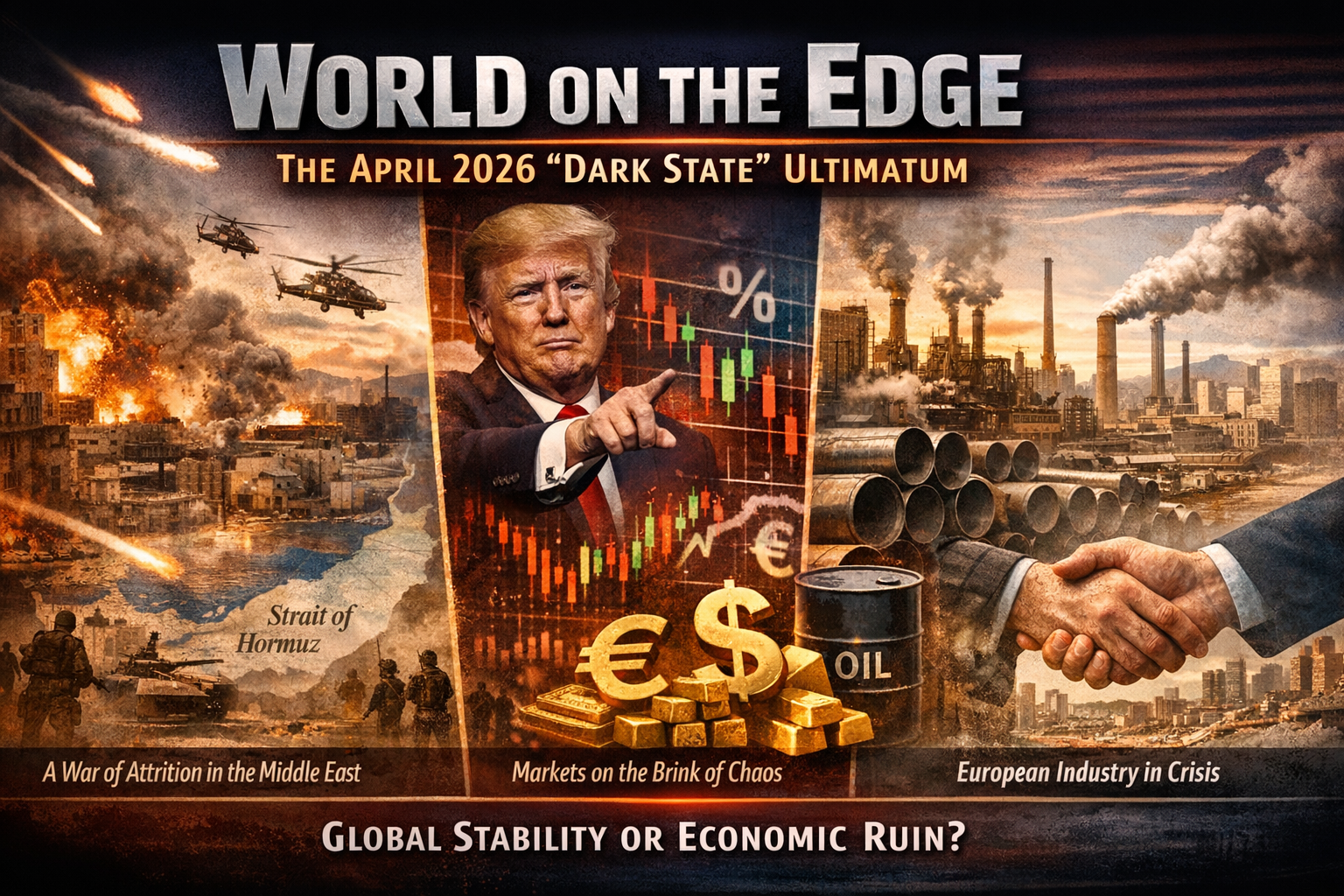

The global order is undergoing a profound and turbulent transformation—one that resembles a full-scale systemic reset. As of April 8, 2026, the Middle East has shifted from a battleground of proxy conflicts to the center of an intense and direct war of attrition. With the U.S.-led “Operation Epic Fury” now in its sixth week and Iran effectively enforcing a blockade over the Strait of Hormuz, the global economy is teetering on the brink.

- The War: From Containment to Leadership Targeting

What began as a contained conflict has escalated into a direct military confrontation. Following the February 28 strikes that severely weakened Iran’s senior leadership, coalition forces have adopted a “decapitation” strategy—focusing on dismantling command structures and critical state functions. Reports indicate a shift away from limited containment toward systematically targeting Iran’s internal security networks and naval capabilities impacting Gulf shipping routes.

In Lebanon, a clear political break has emerged. The government’s decision to expel the Iranian ambassador and distance itself from Hezbollah’s unraveling reflects a major strategic shift. Nevertheless, tensions remain high on the ground, as Israeli forces establish a reinforced buffer zone extending to the Litani River, effectively militarizing southern Lebanon.

- The “Trump Effect”: Rhetoric Driving Markets

Global financial markets are no longer reacting solely to economic indicators—they are increasingly shaped by political messaging. President Donald Trump’s latest speech, described by major outlets as a decisive market catalyst, introduced a firm deadline. His warning of potential escalation toward “Level 3 targets”—including Iran’s civilian infrastructure—if negotiations fail within days has significantly influenced market sentiment.

- Oil: Brent crude has climbed to $114, reflecting a sustained geopolitical risk premium.

- Gold: Meanwhile, gold prices have eased as the U.S. dollar strengthens, becoming the preferred safe haven for investors anticipating a coalition victory.

III. Europe Under Pressure: Industry at Risk

While conflict unfolds in the Gulf, its economic impact is hitting Europe’s industrial core—particularly Germany and Italy. Analysis shows a stark disparity in energy costs, with German manufacturers paying several times more for electricity and natural gas than their U.S. counterparts.

This situation poses a serious threat to key sectors such as chemicals, steel, and aluminum, which are now caught in a “double squeeze” of rising costs and constrained supply. With Qatari LNG shipments disrupted through the Strait of Hormuz, the European Union is approaching an emergency rationing phase that could force factory shutdowns to prioritize household energy needs. As capital flows outward, the euro is increasingly at risk of nearing parity with the dollar.

- The Reconstruction Bet: A Narrow Window of Opportunity

In an unexpected development, a 14-day humanitarian ceasefire brokered through Islamabad has opened a potential path toward de-escalation. This has sparked a new wave of speculative investment known as the “Reconstruction Trade.”

Investors are turning to companies expected to benefit from post-war rebuilding, viewing them as indicators of a possible peace scenario. If negotiations succeed in delivering a comprehensive agreement, these firms could experience significant long-term growth. However, if the ceasefire collapses, markets may face a sharp and sudden downturn.

The Bottom Line:

The region stands at its most perilous moment since 1973. The coming two weeks will be decisive: they could either usher in a period of large-scale reconstruction and recovery, or trigger a deeper crisis that pushes the global economy into prolonged stagflation.

{kind=link}