Analyzing how this might affect the airline industry and European manufacturing

If President Trump’s threat to destroy Iran’s energy infrastructure is carried out, the economic fallout would extend far beyond the gas pump. For the airline industry and European manufacturing, this represents a shift from “high costs” to a “structural crisis.”

Here is an analysis based on the current 2026 market data:

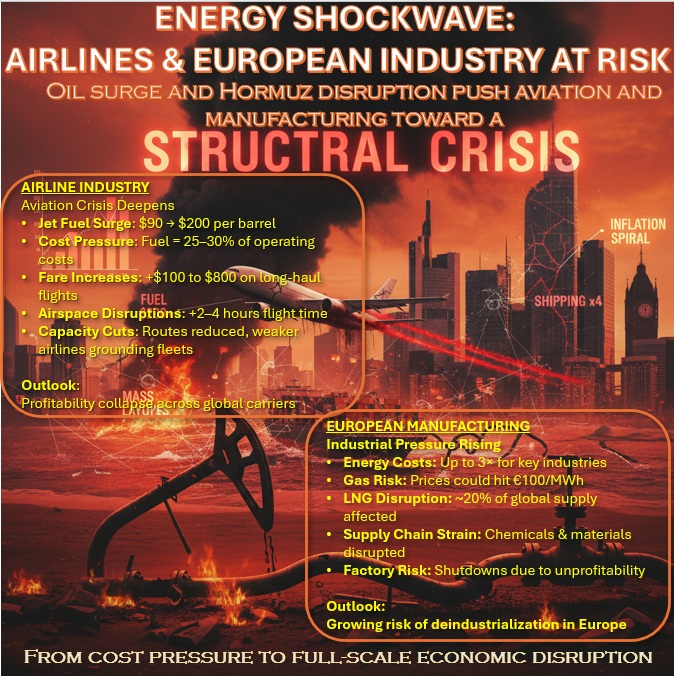

1. The Airline Industry: A Flight to Survival

The aviation sector is currently facing its most severe challenge since the 2020 pandemic. Jet fuel, which typically accounts for 25–30% of airline operating costs, has nearly doubled in price.

- Skyrocketing Fuel Costs: Jet fuel prices have surged from $90 to as high as $200 per barrel in some regions. This has turned a projected $41 billion industry profit for 2026 into a forecasted net loss.

- The “Hormuz Surcharge”: Airlines like Air France-KLM, Cathay Pacific, and Lufthansa have already implemented emergency fuel surcharges. On long-haul flights, passengers are seeing increases of $100 to $800 per round trip.

- Airspace Gridlock: With Iranian and regional airspace closed or dangerous, flights between Europe and Asia are forced into narrow “safe corridors.” This adds 2–4 hours of flight time, further increasing fuel consumption and straining crew schedules.

- Capacity Cuts: Budget carriers and mid-tier airlines are already grounded. United and Air New Zealand have begun cutting “unprofitable” routes, effectively reducing global air connectivity.

2. European Manufacturing: The Deindustrialization Threat

Europe enters this crisis in a fragile state. Unlike the U.S., which is a net energy exporter, Europe relies heavily on imported LNG and oil, much of which is now “trapped” behind the Strait of Hormuz.

- Energy-Intensive Industries at Risk: Sectors such as chemicals, steel, and glass in Germany and the Netherlands are seeing production costs triple. If natural gas prices hit the forecasted 100 EUR/MWh, many plants may face “industrial curtailment”—effectively shutting down because they are no longer profitable.

- The LNG Chokepoint: While Europe has diversified away from Russian gas, it replaced it with LNG from Qatar and the UAE. With the Strait of Hormuz blocked, roughly 20% of global LNG trade is offline. Europe is now in a “bidding war” with Asia for the remaining spot-market cargoes, driving prices to unsustainable levels.

- Supply Chain Collapse: Iran is a major supplier of localized components and materials (like fertilizers and specialized chemicals). The “obliteration” of their infrastructure would permanently break these supply chains, causing delays in European automotive and agricultural sectors.

- Strategic Pivot: In response, the EU is fast-tracking renewable energy. Germany recently added 12 GW of onshore wind auctions, realizing that “home-grown” energy is the only way to shield manufacturing from Middle Eastern volatility.

Summary of Impact

| Sector | Immediate Effect | Long-term Risk |

| Airlines | 20–30% fare hikes; emergency surcharges. | Widespread bankruptcies of non-hedged carriers. |

| Manufacturing | 50% increase in natural gas/power costs. | Permanent relocation of factories to the U.S. or China. |

| Consumer | Reduced travel; higher goods prices. | “Greenflation” as Europe accelerates its energy transition. |

Bottom Line: For airlines, this is a “profitability wipeout.” For European manufacturing, it is an “existential competitiveness crisis.”

{kind=link}